You’re here because someone—maybe your CEO, maybe your investor, maybe your gut—told you that owning payments could be a game-changer for your platform. They’re right. But here’s the part that gets glossed over: how you own payments matters. Should you become a full Payment Facilitator (PayFac)? Or should you partner with a PayFac-as-a-Service provider?

If you’re a CTO, architect, or lead dev navigating this decision, you’re in the right place. We’re going to walk through the differences between going full PayFac and using PayFac-as-a-Service (PFaaS), and why the right decision could be the difference between 6 months of smooth growth—or 18 months of regulatory nightmares.

This isn’t marketing fluff. This is your developer’s guide—straight talk, no filler.

First, What Is a Payment Facilitator (PayFac)?

At its core, a Payment Facilitator is a master merchant that onboards and manages sub-merchants under its own payment umbrella.

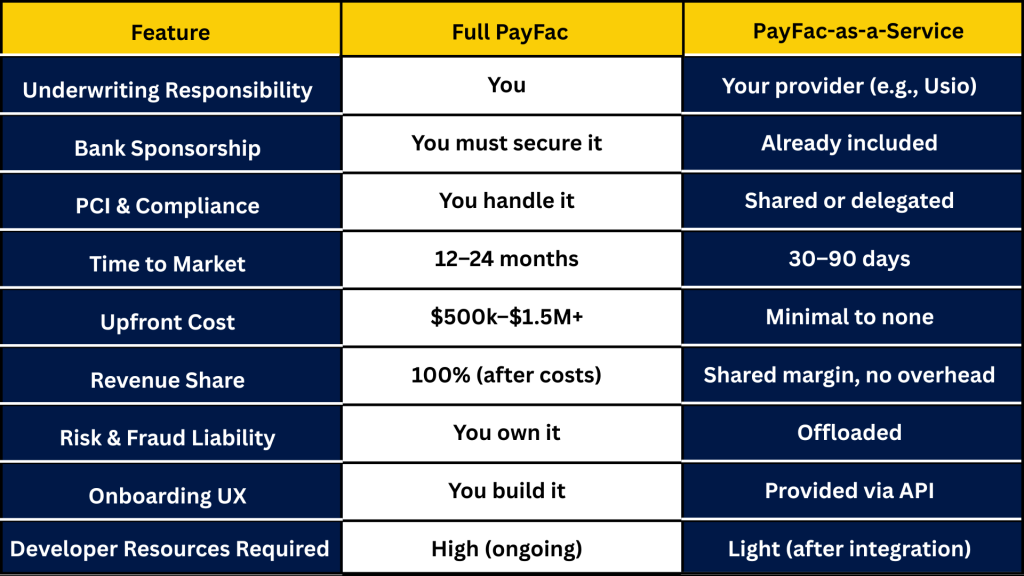

In plain English: You, as the platform, take full responsibility for underwriting, onboarding, monitoring, and settling payments for your customers.

You become the bank’s trusted partner. You control the flow. You take the risk. You (hopefully) make more money.

It’s a serious move. You get:

- Full control over your users’ payment experience

- Ownership of the financial relationship

- Deeper data and monetization opportunities

But also:

- Regulatory burden

- Risk and compliance headaches

- 12+ months of build time

- ~$1M+ upfront cost

What Is PayFac-as-a-Service?

PayFac-as-a-Service gives you all the benefits of embedded payments—but without the regulatory weight and operational lift.

Instead of becoming a registered payment facilitator yourself, you work with a company (like Usio) that already is one. You integrate their API, and your customers are onboarded as sub-merchants under their sponsorship, not yours.

It’s like renting the infrastructure instead of building the entire highway system.

Side-by-Side: PayFac vs PayFac-as-a-Service

️

Let’s Talk Tech: What the CTO Cares About

1. Integration Complexity

If you go full PayFac, you’re not just integrating with a gateway. You’re building an entire financial infrastructure. Think:

- KYB/KYC automation

- Real-time fraud detection

- ACH and card payment rails

- Bank sponsorship APIs

- PCI vaults

- Dispute management systems

- Treasury and settlement engines

You’re essentially building a FinTech company inside your SaaS company.

With PFaaS? You plug into one API. Usio, for example, offers:

bash

Copy Edit

POST /api/merchant/onboard

POST /api/payment/card

POST /api/payment/ach

POST /api/disbursement

Everything else? Pre-built. Abstracted away. Done.

2. DevOps Load

Full PayFac = maintaining compliance pipelines, audits, downtime SLAs, fraud alerting queues, and reconciliation systems.

PFaaS = integration and occasional tweaks. You focus on product. We focus on payments.

Monetization: Who Makes More?

Here’s where it gets nuanced.

Going full PayFac can be more profitable—if you hit significant scale and have the capital to invest upfront.

But that margin comes at a cost:

- Fraud and chargebacks eat into your revenue

- Compliance teams aren’t cheap

- Regulatory audits and fines are real

PFaaS gives you a generous revenue share (often up to 80–90% of the net margin), but without the cost of building and running the operation. Usio, for instance, pays out monthly revenue share to partners and developers. Stripe, by comparison? Zero, unless you’re a processing giant.

Pro tip: With PFaaS, you’re profitable at a few thousand monthly transactions. With full PayFac, break-even could take years.

Risk Management and Compliance

When you become a full PayFac, you step into the regulatory ring with gloves off:

- You file for registration with card brands (Visa/Mastercard)

- You get underwritten by a sponsoring bank

- You become liable for sub-merchant fraud

- You may be subject to state money transmitter laws

You also need a compliance officer, a fraud mitigation team, and possibly legal counsel. Not optional.

With PFaaS, your provider handles:

KYC/KYB checks

Bank compliance

Transaction monitoring

PCI compliance

Disputes and chargebacks

You get visibility, not liability.

️

Developer Experience: What Will You Actually Build?

If You Go Full PayFac:

You’ll build…

- A full onboarding flow with risk scoring

- A backend for merchant document uploads

- An integration with a gateway or processor (or both)

- Reconciliation and settlement reporting

- Alerting and audit logs

- Admin tools for your support team

It’s fun if you like a challenge. Not so fun when your CEO wants payments live in Q3.

If You Choose PFaaS:

You’ll build…

- A clean onboarding UI tied to our onboarding API

- A payment screen calling a single Usio endpoint

- Optional disbursement or print/mail logic

Boom. Live in weeks.

Real-World Use Cases: When to Use Which

Go Full PayFac If:

- You process $1B+ in payments annually

- You have a dedicated payments team (compliance, ops, dev)

- You want to build proprietary risk and fraud systems

- You’re okay waiting 12–18 months to go live

- You’re looking for ultimate control and margin

Choose PFaaS If:

- You want to monetize payments in 60–90 days

- You don’t want to build and maintain compliance infrastructure

- You’re looking for developer-friendly APIs and support

- You want a shared revenue model with no risk

- You’d rather focus on product than payments

What You’ll Need to Get Started (Either Way)

Going Full PayFac:

- $1M+ in budget

- 6–8 devs (for 12+ months)

- Compliance officer

- Legal review

- Bank sponsorship

- Payment operations team

- High transaction volume to justify it

With PFaaS:

- 1–2 engineers

- A payments roadmap

- A sandbox account

- A quick call with Usio’s dev team

- Your first onboarding in a week or two

Switching from Stripe or Others? We’ve Got You.

Stripe doesn’t offer true PayFac. They offer Stripe Connect. No revenue share unless you’re massive. No control. No love for mid-sized SaaS.

At Usio, we’ve migrated platforms from Stripe, Finix, Payrix, and Worldpay. Our team handles:

Token migrations

Sub-merchant mapping

API adaptation

Data validation

Fraud policy handover

You get a clear path, full support, and direct access to engineers—no ticketing queue.

Final Thoughts for the CTO

Becoming a Payment Facilitator is a career-defining decision. It’s not just a technical challenge—it’s a business transformation. You’re not just building features. You’re becoming a financial institution.

That may be the right move. But it also might not.

If you’re focused on time to market, developer efficiency, and maximizing revenue without maxing out your team, PayFac-as-a-Service is likely your best bet.

Especially when the partner is Usio.

TL;DR

- Full PayFac = More control, more margin, massive complexity

- PFaaS = Fast launch, shared revenue, no risk, and minimal code

Choose full PayFac if you have:

- $1M+ in capital

- 12+ months of dev time

- A tolerance for regulatory burden

Choose PFaaS if you want:

- Revenue share without risk

- Integration in weeks, not years

- Direct access to real devs (hi )

Ready to Build Like a PayFac—Without Becoming One?

Usio’s PFaaS solution gives you:

- Single API for cards, ACH, disbursements, Text2Pay, and print/mail

- Automated merchant onboarding

- Revenue share paid monthly

- In-house tech stack (no third-party failures)

- Direct access to our developer team 5 days a week

Let’s build something smart together.