Integrated Payments

Made Simple

Everything you need to determine if you should build your own payments platform or outsource to a payments partner.

Table of Contents

i. Overview

ii. Must-Haves Before Processing

iii. Step by Step Instructions

iv. Reasons to Work With Usio

Overview

In this guide, we’ll explore the key elements needed to create your own payment platform. By the end, you’ll understand the costs, risks, and essential steps. Our goal is to help you decide whether your business should build an in-house payment solution or partner with a payment processing service.

First things first: To set up your integrated payment platform, you’ll need to become a Payment Facilitator. We’ll mention this term often throughout the guide.

What is a Payment Facilitator: A payment facilitator, often abbreviated as “PayFac,” is a type of financial intermediary or service provider that enables businesses to accept payments from customers. Payment facilitators simplify the process of accepting electronic payments, such as credit card transactions, for smaller businesses, software platforms, or other organizations that may not have the resources or infrastructure to set up their own merchant accounts with payment processors (acquirers).

Before you process one dollar here are the must haves...

1

Find a processor who will sponsor you as a Pay Fac with a Member Bank and

Pass an extensive underwriting process.

2

3

Cash Reserves

In most cases, put up substantial cash reserves and personal guarantees with the bank or processor. Additionally, you must develop credit underwriting guidelines and AML policies.

4

Ensure you have the internal capabilities and infrastructure required to manage settlement funds to your downstream clients, also referred to as merchants.

Hire staff who are experts in merchant acquiring to sell, implement, support and manage the day-to-day activities of the payments

5

6

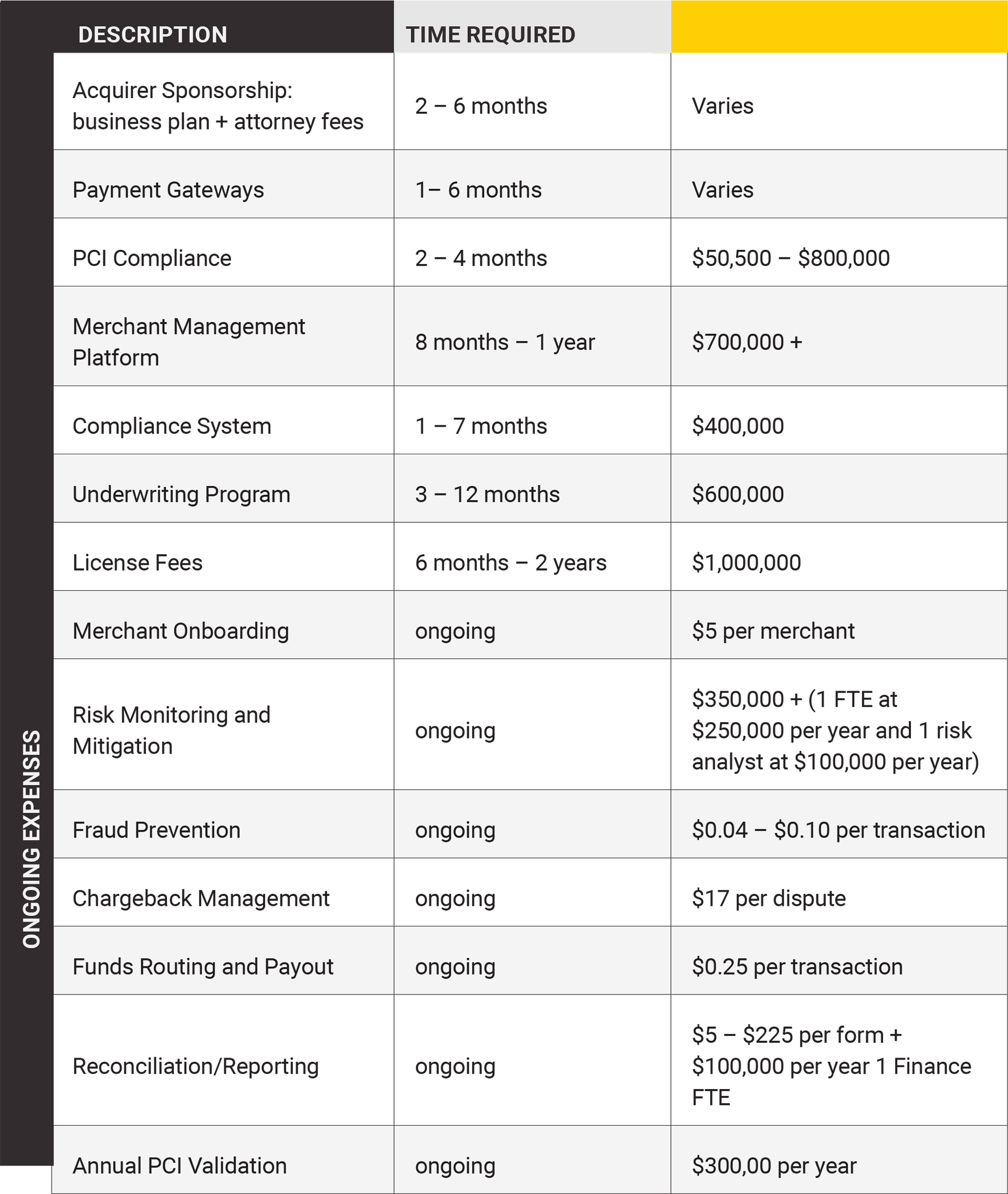

Ensure that payments operations are in (and remain in) full compliance with PCI & other mandates, which can cost hundreds of thousands of dollars annually.

Risk 101

Becoming a PayFac requires building and investing in multiple systems. PayFacs have ongoing legal requirements to maintain their good standing and credit requirements with acquiring banks and card networks.

The Electronic Transactions Association (a professional advisory group from payment processors, banks and card networks) strongly recommends engaging these industry experts and legal counsel to ensure compliance and adherence to laws and guidelines.

It’s estimated that payment fraud increases at a rate of 41% every two years.

Roughly 40% of consumers who commit fraud will do it again within 60 days

Roughly 40% of consumers who commit fraud will do it again within 60 days

Step By Step

STEP ONE

Banks & Sponsorship

Find an acquiring bank: as a PayFac, you must approach acquiring banks with a business plan to establish a partnership. Next, get sponsored to facilitate payments for sub-merchants

STEP TWO

Integration

Integrate your payment platform and gateways to provide functionality for sub-merchants to process online payments.

STEP THREE

Certification – It’s the law

Obtain Level 1 PCI certification to ensure the security of data. You are required by the Payment Card Industry Data Security Standard to be certified, which may also include Mastercard and Visa (EMV or chip) certification if the PayFac supports in-person transactions.

STEP FOUR

Onboarding & Compliance

Create underwriting policies and systems to ensure only legal entities that comply with card network and acquirer rules are onboarded. Your system and employees must:

Estimate the nature of sub-merchant’s financial health and risk, including, compliance issues, fraud, credit, regulatory and reputational risk.

Verify identities of each sub-merchant, including KYC, owner structure and other business details.

Check OFAC and MATCH lists for sub-merchants before onboarding. Mastercard manages the Member Alert to Control High-Risk Merchants (MATCH) list.

STEP FOUR

Onboarding & Compliance

Obtain Level 1 PCI certification to ensure the security of data. You are required by the Payment Card Industry Data Security Standard to be certified, which may also include Mastercard and Visa (EMV or chip) certification if the PayFac supports in-person transactions.

- Estimate the nature of sub-merchant’sfinancial health and risk, including,compliance issues, fraud, credit, regulatoryand reputational risk.

- Verify identities of each sub-merchant,including KYC, owner structure and otherbusiness details.

- Check OFAC and MATCH lists for sub-merchants before onboarding. Mastercardmanages the Member Alert to Control High-Risk Merchants (MATCH) list.

STEP FIVE

Internal Systems

To mitigate risk, you will need to a build a system with internal policies to conduct due diligence. Your PayFac system and staff will need to:

Comply with each AML law by encoding rules and requirements from card networks and regulatory organizations.

Identify suspicious activities (including indicators of terrorist financing).

File Suspicious Activity Reports with the Financial Crimes Enforcement Network (FinCEN) or acquirer, as required.

STEP SIX

Registration & Licenses

Submit registrations and apply for any additional required licenses such as:

- Register as a PayFac with each card network.

- Apply for money transmitter licenses (MTLs) in each state the payfac operates in (if required to support certain fund flows).

STEP SIX

Merchant Systems

Build automated merchant dashboards, payoutsystems and dispute management processes tohandle chargebacks.

Every sub-merchant: Verify the identity, business model and owner information for each sub-merchant. Set up payments processing for sub-merchants.

Update and Monitor risk systems: Perform due diligence, monitor sub-merchant activity on an ongoing basis and mitigate risk as needed (e.g., apply processing caps, delayed funding, or reserves)

Prevent and block fraud: Proactively prevent fraud on the platform and block or review suspicious transactions. Best practices include using adaptive machine learning for fraud detection. Submit evidence to card networks when needed for chargebacks on behalf of sub-merchants.

Pay out funds to sub-merchants: Ensure sub-merchants are paid their earnings on time.

Reporting and reconciliation: Generate and distribute 1099s or other tax forms as needed annually.

Maintain PCI DSS compliance: Ensure the platform remains compliant even as data flows and the customer experience evolves. Some card networks require PayFac’s to submit quarterly or annual reports, or complete an annual on-site assessment to validate ongoing compliance.

Renew PayFac registration and licenses: Re-register as a PayFac with card networks annually and update or renew MTLs on the required cadence.

There's an Alternative Solution

To summarize, there is a significant amount of time and money needed to become a PayFac. With Usio, software companies receive the benefits and functionality of being a PayFac without taking on the responsibility, liability, operation infrastructure and more.

Reasons To Work With Usio

Whether your application demands a hosted Pay page or you require the flexibility of taking payments mobile, we have a solution for that! Usio is an innovator of cutting-edge payment applications and technologies. Our SDKs, with full code, are written for each API in the newest and most common coding languages

WHAT MAKES US UNIQUE

Our automated enrollment tool eliminates the onerous process required to set up merchants. With our unique boarding API you can board one merchant at a time or 1,000s. We are the only payment company that offers this level of flexibility

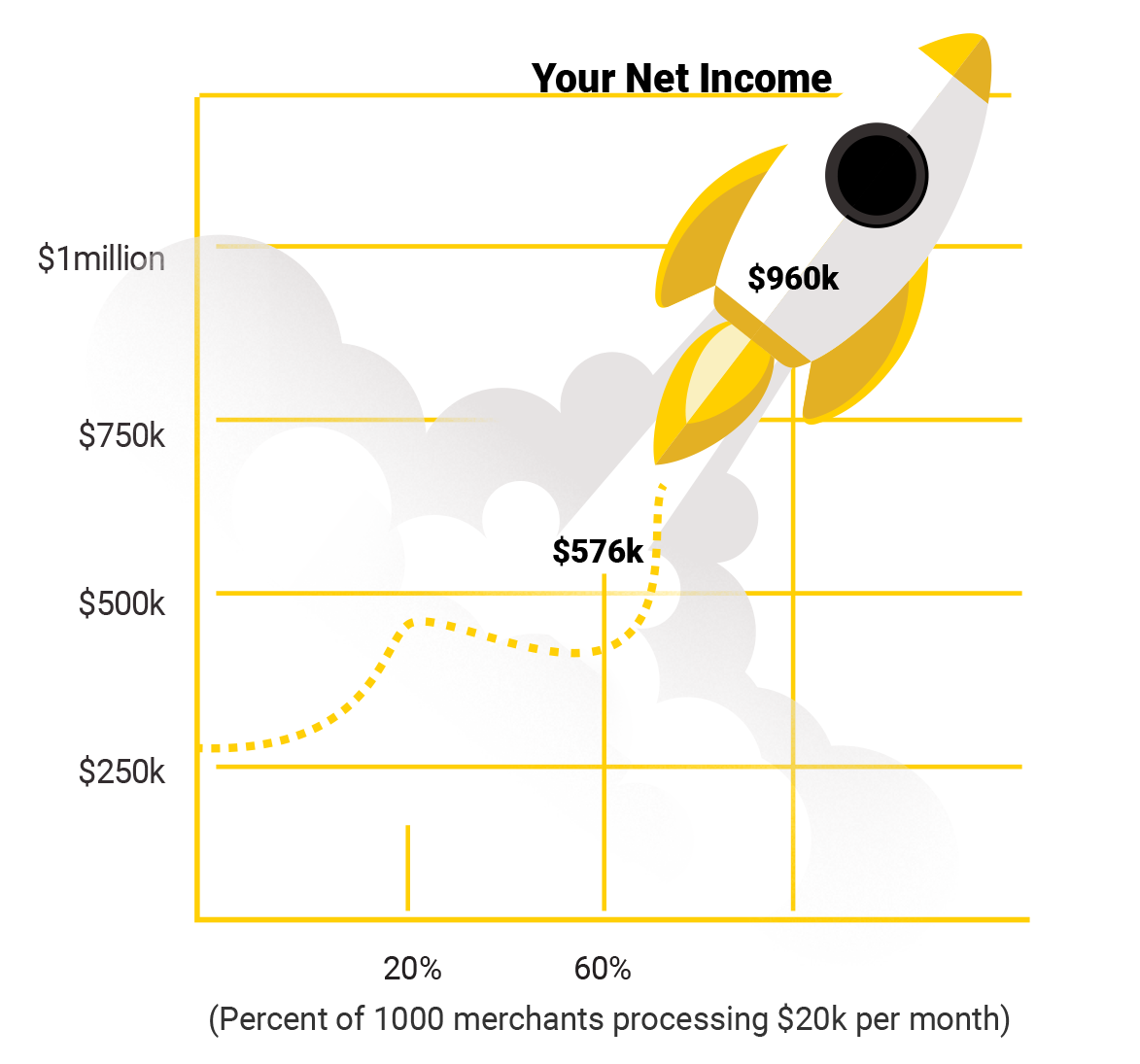

Like every business out there, software companies are always trying to find ways to earn incremental new streams of recurring revenue. Even if you currently have a payments solutions in place, how many of your users are actively using it? To put that in perspective, let’s assume that you have 1,000 merchants using your software. Chances are you are not earning any residual income on even 10% of them. What if there is a simple way to move that 10% to 80% or more of your users. Would that be of value to you? Below is a realistic example of how Usio will dramatically impact your bottom line simply by partnering with us. We do all of the heavy lifting, directly increasing your net income.

Let’s say you have 1,000 merchants currently using your software and 80% start processing payments (800 merchants.)

Those 800 merchants process $20,000each per month for a total of $16mm in processing volume every month.

That $16mm turns into a net take-home income of $64,000 per month, or $768,000 per year for you. That is right, we said $786,000 per year in your pocket.

Discover how this Software Company is monetizing payments and increasing revenue simply by integrating to the Usio Payment Facilitation platform.

This software company provides an all-in-one giving platform, accounting module, including management software, and mobile applications. These solutions allow companies to better serve their members, empower volunteers and serve their communities.

The Challenge

Prior to their relationship with Usio, this company was not generating any revenue from the payments flowing through their software, nor were they receiving adequate customer support for any issues that occurred. They wanted a way to control their own destiny, but knew doing so would either require them to become a Payment Facilitator or leverage a platform like Usio. They quickly determined shouldering the burden of risk, compliance, finding a sponsor bank and spending 12-18 months and $3-5mm to develop a platform was something they didn’t wish to undertake.

Companies come to us because they want fewer software tools. Providing a comprehensive solution is paramount to our growth since our customers operate primarily off of charitable contributions. Offering a robust giving platform is a must for this software company.

– Usio Co-founder

- USIO INTEGRATED PAYMENTS

Usio provided all the Payment features and functionality This software company needed without taking on the risk and compliance concerns, investment or the need for payments expertise. The well-documented Usio API’s allowed This software company to integrate quickly—within two days— and begin monetizing payments soon thereafte

- When payment concerns or questions about refunds, payment types, etc. arise, Usio responds immediately. With Usio, the software users have direct access to customer support, including personal mobile numbers in case of an emergency.

- EXPERTISE Following Usio best practices and recipes for success, This software company communicated to their end-users the benefits of an integrated solution and the ease of onboarding. This yielded in 86.6% of their customer base adopting the integrated giving solution. CUSTOMER SUPPORT

- INCREASED REVENUE

This software company now earns additional revenue from payments and offerings running through their system via Usio. In fact, almost one-third of This software company’s revenue is now derived from payments.

About Usio

Usio, trusted with billions of dollars in transactions, is a leading fintech payment solution. The Usio Platform delivers the most secure, simple and cost effective payment experience for our partners and their customers. From online, to in-line, mobile and traditional solutions, Usio payment methods include: credit/debit card, ACH, Remotely Created Checks, and cryptocurrency. Usio services include: Payment Facilitation, Text2Pay, prepaid card issuing, printing/mailing, hosted payment pages, electronic bill presentment/payment, account verification, and recurring billing. Plus, Usio holds the unique distinction of being in business for more than 20 years and is just one of few who is Nacha Certified.